It’s fair to say that I never wanted to write this blog. I was at PDAC all last week and I hoped that this subject would go away. Unfortunately it doesn’t look like it is, so here I go. It feels a little wrong to be writing a blog about materials that will benefit from a war in which people are losing their lives, but unfortunately it has been going on for long enough now that it’s becoming difficult to ignore.

I remain hopeful that the politicians will get their acts together and this blog will be moot but, just in case they don’t, here are my thoughts on which materials should benefit if the current situation in Iran and the Middle East is not resolved quickly.

In my view there are three tiers of materials that are affected by the attacks:

- Tier 1: Materials whose supply is directly impacted

- Tier 2: Materials where oil & gas price increases may impact

- Tier 3: Materials whose demand may be impacted if hostilities go on for a long period

Tier 1 materials

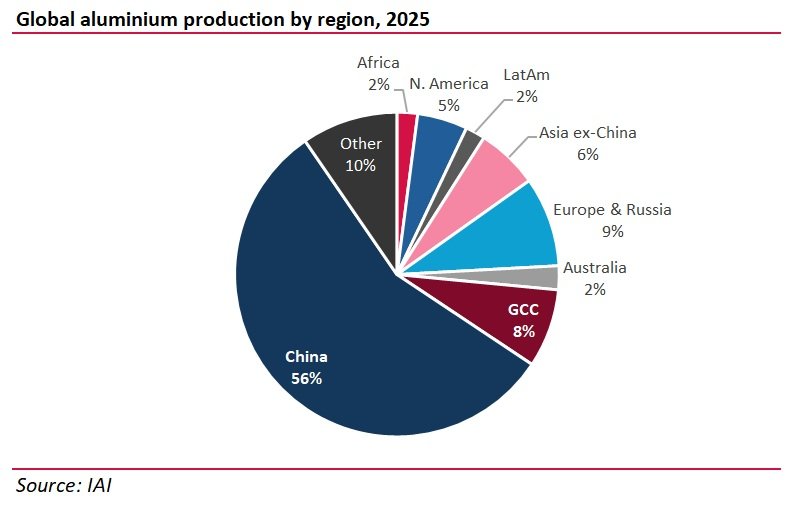

The obvious materials here are oil and gas, which everyone is talking about. I won’t talk about those. Instead I want to talk about another material; aluminium. In my blog from September last year, I talked about aluminium and why I thought aluminium should go on a run. One of the subjects I talked about was China’s decision to cap aluminium output. I highlighted that the only other regions that were seeing rapid aluminium supply growth were the GCC and Indonesia. I noted that GCC is 9-10% of global aluminium output and has been one of the fastest-growing output regions in recent years.

Last week Aluminium Bahrain, one of the world’s largest smelters at 1.6Mtpa, declared force majeure on shipments due to disruption in the Strait of Hormuz, and Norsk Hydro decided to shut down its 648Ktpa smelter in Qatar, which could take up to a year to restart. Most smelters in the GCC region rely on alumina imported from elsewhere, so it’s possible, if not likely, that other smelters will have to stop producing as well. And, if they do so, like Qatar, restart could take an extended period of time.

Some industry specialists are starting to talk about aluminium as a material to benefit from disruption caused by the war, but discussions on O&G are much more widespread. This is a flag to my readers to keep an eye out on aluminium. Last week, when I got back from PDAC, I went right out and bought a physical aluminium ETC. That’s how sure I am about this.

Tier 2 materials

The material that’s gaining all the column inches and that everybody is talking about in this tier is nitrogen fertiliser. But I want to throw another two materials into the ring.

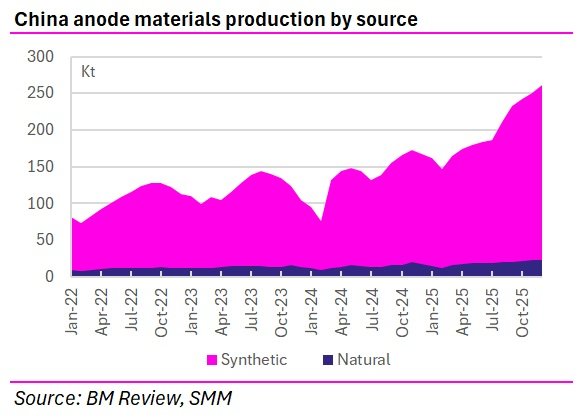

First up is natural graphite anode material and, by extension, potentially natural graphite as well. Here’s how my thinking goes.

Some years ago we were really excited about the potential for strong demand for spherical graphite in the battery industry. It looked as though technical advances were allowing it to gain market share from more highly-priced synthetic graphite and it was going to be an exciting material for the next decade. But then China added a lot of synthetic graphite anode capacity. So much that synthetic graphite prices, which had been trading at a large premium to spherical graphite anode prices, dropped substantially and became competitive with spherical graphite anode material prices. This pushed spherical graphite prices down as well and impacted growth for spherical graphite demand and hence prices for flake graphite.

But oil and hydrocarbons are major input costs for synthetic graphite production. With oil prices up substantially, that should impact the cost of needle coke and petroleum coke. That should drive synthetic graphite anode prices up and should – at last – lead to higher prices for spherical graphite and natural graphite. Now, one caveat. Power/heat are also key for production of most anode materials, so it won’t be all easy but, in my view, higher oil prices should support this segment, which has struggled for some time.

And I want to throw one other possible material in there…lithium. You might think this is a reach, but let me just work through my logic. Could high oil prices provide a demand catalyst for EVs? I think they could, particularly in countries and regions that are not highly exposed to LNG imports from the GCC region. For instance, let’s think about China, the world’s largest EV market. Only c.3% of power production comes from LNG, the balance coming from coal and an increasing amount of renewables. Could high gasoline prices therefore result in a bump in consumer demand for EVs? Such a move would come at a great time for Chinese EV manufacturers, which have been struggling with slowing demand growth.

Those countries which are most exposed to LNG as a power source are, interestingly, those with relatively small EV markets…Japan and South Korea come to mind. Europe is an interesting situation – it has about a 20% exposure to gas in power, BUT less so in the summer when renewables tend to dominate. The US is a gas exporter and is highly-exposed to higher gasoline prices, so could EVs get a second wind there? And then some of the fastest-growing EV markets in the world, like Australia and Canada and Latin America also have low exposure to LNG in their power grids.

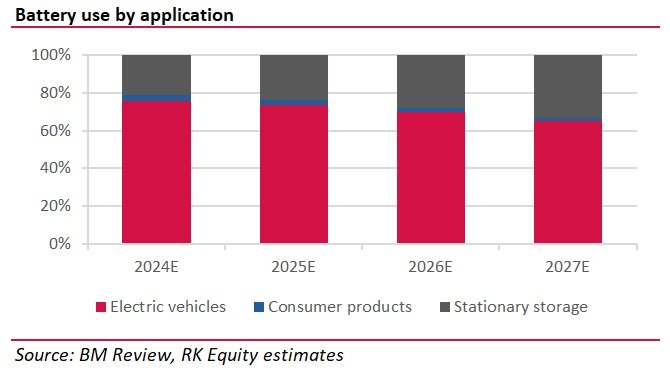

So, is it a stretch to think that a prolonged period of high oil prices could put EVs in focus for consumers again? And, if that does occur, would an acceleration in EV sales be enough to offset the deferment of GCC BESS projects? Well, it’s a no-brainer that an acceleration in EV sales would offset any weakness in BESS. EVs are still the biggest consumer of batteries in the world by a fair distance. So, if that’s the case, the major beneficiary of an increase in battery demand is likely to be lithium…

Tier 3 materials

Nobody is really talking about this segment as yet. But the longer these actions go on for, the more pressure that’s likely to cause on the supply/demand balance for a number of materials, in my view. Let’s talk about a few products.

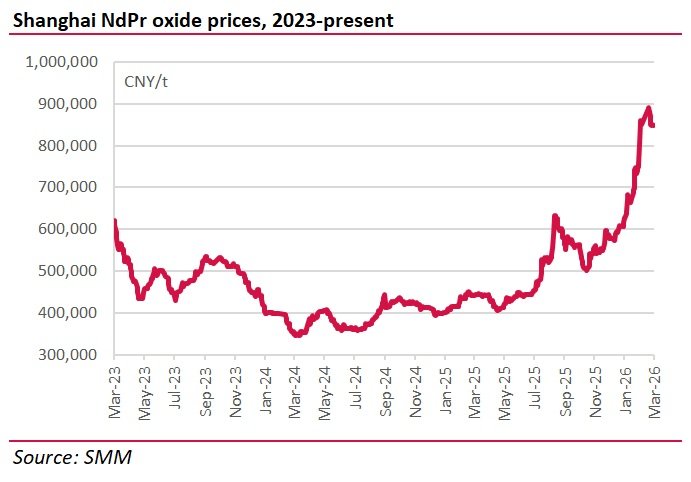

Drones, for instance. They are one of Iran’s primary offensive weapons, and are also used extensively by Russia and Ukraine. They use a lot of rare earth magnets, which use a lot of rare earth metals. And let’s not forget guided weapons and defensive weapons like missiles which all rely on rangefinders which use heavy REEs extensively. Demand for REE was already being impacted by the war in Ukraine. As the war in Iran extends further and further, what will that do to REE demand? REE prices in China have been rising substantially since the back end of last year, but we haven’t really seen share prices of REE producers and developers react in any significant way to this.

Munitions use a number of metals but those metals in which munitions constitute a substantial share of global demand are a much smaller list. And they can be summarised in two materials; antimony and tungsten. Antimony is used in primers and detonators, flame retardants and ammunition. Tungsten is used in armour-piercing ammunition in particular. Supply in both metals is dominated by China and hence western users are substantially at risk from China turning off the taps. Equities in both areas ran strongly last year. Antimony stock performance has corrected significantly but tungsten stock performance is still relatively strong. But perhaps it’s time to have a look at both once again.