In the past 12 months there have been a number of examples of a substantial disconnect between physical commodity prices and paper commodity prices.

Commodity exchanges were historically set up to solve a very practical problem for producers and consumers of commodities. In the early days, producers and consumers faced volatile prices, inconsistent product standards, and high counterparty risk. Exchanges introduced standardised contracts, grading systems, and centralised trading venues, which allowed buyers and sellers to agree on prices in advance (via futures), hedge risk, and ensure reliable settlement.

Over time, they evolved first into price discovery mechanisms for global markets, and then into venues for financial speculation.

But has that evolution now gone too far?

From price discovery to price distortion

At their peak, commodity exchanges represented a genuine aggregation of market knowledge. Prices reflected the marginal balance of supply and demand, informed by those closest to the physical market – producers, consumers, traders and merchants.

Today, that balance appears to have shifted.

Financial participants – hedge funds, systematic strategies, ETFs and increasingly state-linked capital – now dominate volumes across many commodity markets. In some cases, the scale of financial flows dwarfs the underlying physical trade. This raises a fundamental question:

Are commodity exchanges still discovering prices, or are they increasingly setting them?

The distinction matters. If prices are set by financial positioning rather than physical fundamentals, then the core purpose of exchanges – efficient risk transfer between producers and consumers – begins to erode.

Evidence of disconnect: recent market behaviour

Across multiple commodities, the past year has produced examples where paper pricing has diverged meaningfully from physical conditions.

Oil

This is perhaps the clearest example, certainly in recent weeks. Since the current Iran War was initiated, physical oil prices in some parts of the world have nearly doubled. Paper prices haven’t. Indeed, the US government has admitted to shorting large amounts of oil contracts on exchange to keep prices down. As has the Japanese one. If that’s not evidence of attempts to supress price discovery, I don’t know what is.

Oil products

We see a similar situation in oil products. Oil product physical prices are trading at a substantial premium to paper prices, reflecting a substantial shortage in most markets. Again, it seems like financial players with deep pockets are outspending producers and consumers to make prices appear lower.

Copper

Copper has exhibited a more subtle but equally important divergence. Financial markets continue to price a structural deficit narrative tied to electrification and energy transition. Yet physical markets – particularly in China – have recently shown softness, with rising inventories and weaker spot demand. The result is a persistent tension between long-term financial positioning and short-term physical reality.

Gold

Gold presents a different form of disconnect. Here the divergence is not so much between futures and spot, but between financial claims and physical metal. Elevated premiums for physical gold, alongside strong central bank demand, suggest that the marginal buyer recently has increasingly valued possession over exposure.

Silver

The past several months have exhibited tight local physical conditions which have not been fully reflected in broader futures pricing, again pointing to a mismatch between financial flows and physical fundamentals. Indeed, there have been periods where short attacks have taken place in low volume hours on exchange, which certainly seems to point to some level of financial market manipulation.

Lithium carbonate

We have seen extremely active trading in Chinese lithium carbonate futures which has highlighted the difference between Chinese prices, taking place within a partially-closed capital system and reflecting domestic supply/demand and policy, compared to global pricing structures.

China vs the West: two price systems

Chinese exchanges (SHFE, GFEX, INE) operate within a partially closed capital system, where flows are restricted and domestic fundamentals dominate pricing. Western exchanges (LME, COMEX, ICE), by contrast, are globally arbitraged and heavily influenced by financial capital.

The result is effectively two parallel price systems:

- A China price, reflecting domestic demand, policy and inventory

- A global price, reflecting financial positioning and expectations

These systems can and do diverge for extended periods. In metals such as copper and aluminium, Chinese prices have frequently traded at a discount to LME equivalents, reflecting weaker domestic conditions even as global prices remain supported. Over the course of the past year, COMEX copper prices have traded at a substantial premium to Chinese ones.

This is not a temporary issue; it’s structural. And is set to get even more structural as Western countries seek to build their own supply chains.

The rise of state intervention

If the increase in importance of financial traders has complicated price discovery, the increasing involvement of governments risks distorting it further.

Strategic stockpiling, coordinated buying programmes and, in some cases, direct participation in futures markets, mean that prices are no longer purely the outcome of commercial hedging and speculative positioning. They are also instruments of policy.

When governments deploy capital into commodity markets, the line between hedging, speculation and intervention becomes blurred.

At that point, it is reasonable to ask whether prices still carry meaningful information?

Are paper prices being manipulated?

“Manipulation” is a loaded term, and often misused. Markets are, by definition, influenced by participants with differing objectives and varying levels of capital.

But there is a difference between influence and distortion.

If prices are consistently driven away from physical reality by flows that are:

- disconnected from underlying supply and demand

- amplified by leverage

- or motivated by policy rather than economics

Then surely the signal embedded in those prices becomes less reliable?

In such an environment, producers and consumers face a paradox: the very instruments designed to reduce uncertainty may be increasing it.

What does this mean for industry?

For producers, distorted prices can lead to:

- misallocation of capital

- over- or under-investment

- difficulty in securing financing tied to unreliable benchmarks

For consumers, it can mean:

- hedging becomes less effective

- input costs become less predictable

In both cases, the link between the financial market and the physical reality weakens.

Is there an alternative?

One potential response is a shift back towards physically anchored pricing mechanisms. In the modern world, it is increasingly feasible for buyers and sellers to transact directly, using:

- long-term contracts

- index-linked pricing

- or even bilateral negotiated benchmarks as we see in many other commodities

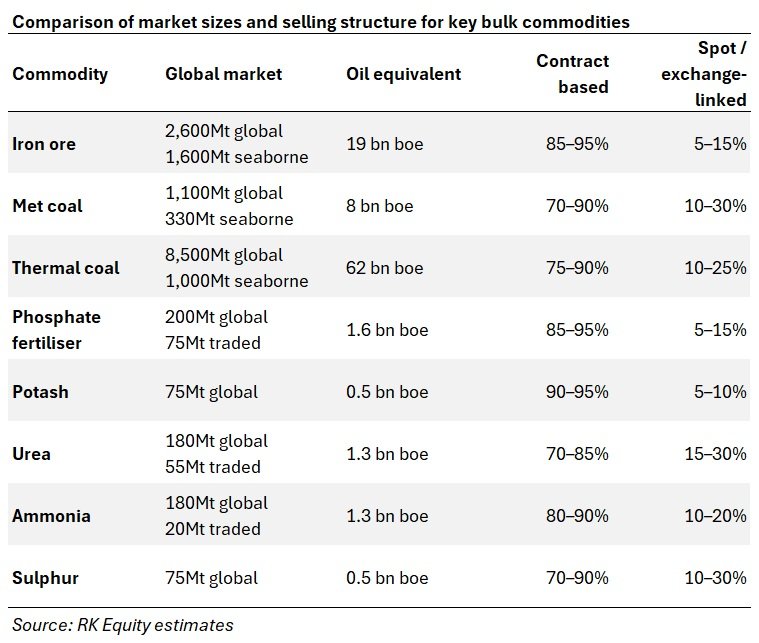

Arrangements like this can help to reduce volatility, better reflect regional market conditions and align pricing more tightly with physical flows. And indeed a big chunk of global bulk commodity trade still sits under this structure. Commodities such as thermal coal, iron ore and fertilisers still utilise buyer-seller contracts for in excess of 70% of their trade.

If we compare the markets featured in the table above with oil, we find that the oil market is c.5Bt, smaller in size than coal, but bigger than all of the other bulk materials. So it would be viable to take oil off exchange, although it would still be a major move.

However, the use of buyer-seller contracts does come with trade-offs:

- less liquidity

- reduced transparency

- greater challenges in financing and risk transfer

Another, more radical, idea is to restrict exchanges to contracts backed by physical delivery. This would limit leverage and reconnect pricing to real supply and demand, but at the cost of significantly reducing market depth and participation. This would be a good middle of the road approach between taking commodities off exchange all-together and leaving them on, but directing pricing power back to producers and consumers.

Conclusion

Commodity exchanges were created to serve industry and consumers by reducing uncertainty, facilitating trade, and enabling efficient risk management.

They have evolved into something far more complex: global financial markets where physical commodities are often just the underlying reference point for large-scale capital flows. The increasing pricing volatility we’ve seen on exchange just highlights this.

The question is no longer whether these markets function, but who they serve. Volatility in pricing is a negative outcome for both producers and consumers.

And the answer seems to be increasingly that exchanges serve “financial participants and policymakers” rather than “producers and consumers”. If that’s the case, then surely it’s time to reconsider the model?

We don’t necessarily need to dismantle it, but certainly to rebalance it. Either exchanges with compulsory physical settlement or monthly producer to consumer price contracts utilising price discovery agencies for transparency would be a move in the right direction in my view. Sticking with the current model seems to benefit the few rather than the many.