If you’re not in silver, why not?

First up I should say that for most of my career, I’ve been wary about investing in precious metals. I’ve always preferred materials where I could forecast demand and that hasn’t been precious metals, which tend to trade according to a whole different set of drivers to industrial metals. So, for me to be invested in silver is, in itself, a big thing. For me to be recommending silver as a commodity to other people is an even bigger thing.

And it wouldn’t be happening if something major wasn’t happening in the silver market.

Silver demand (ex-investment) is growing again

For most of my career as an analyst, silver has been regarded as gold’s poorer brother. It moves roughly in line with the gold price, but tends to be a lot more volatile and a large amount of industry specialists only pay attention to the gold/silver ratio in order to ascertain whether silver looks interesting as a long or a short.

Silver’s industrial properties and industrial uses have been kind of by the by since the 2000s when it was clear that printed photographs were in decline. While it’s still used in jewellery and household items, even that segment has been in decline in recent years. And, indeed, physical silver demand itself was in decline until the early part of this decade.

And then something changed. Something big.

It had been known for some time by industry experts that silver was a major component of solar panels, but it was a relatively small market representing less than 10% of global silver demand. And then solar installations went ballistic. And it wasn’t only solar; because of silver’s conducting properties it’s also in demand for other electrical applications like EVs and some grid and electric power applications as well. All of which are also fast-growing markets. Solar demand for silver is set to more than double between 2018 and 2025E.

Which means that ex-investment demand, silver demand is growing again. It’s not growing fast, but it is growing. And that’s very relevant. Because supply is struggling to keep up.

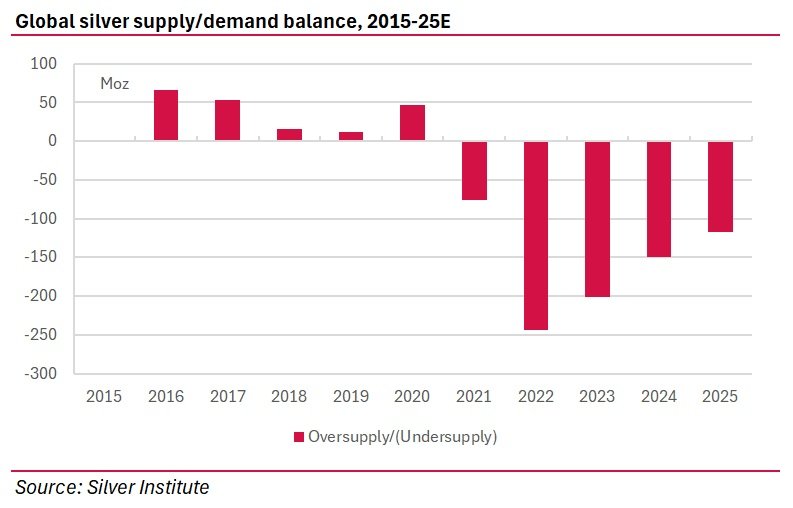

Silver supply is less than demand

I say above that silver supply is struggling to keep up. Actually it’s struggling full stop. Because silver has been in structural undersupply since 2021.

We have to get to the heart of the global silver industry to understand why this is the case. And it really comes about because only 20-25% of mined silver supply comes from actual silver mines. The rest of global silver supply comes from mines that are primary producers of other metals and where silver is a by-product.

And with 75-80% of silver being a by-product, you probably won’t find gold, copper and lead/zinc mines increasing production so that they can raise production of silver. Particularly in an environment when silver prices are performing less well than their primary commodities. And that’s the environment we’re in for many of the silver co-product commodities, such as gold and copper. And that’s why the silver mining industry is struggling to keep up.

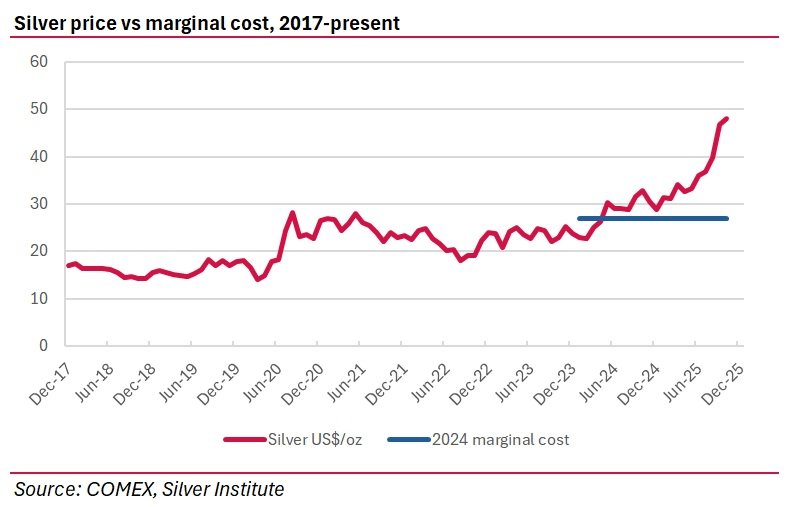

Until recently, the silver price wasn’t enough to incentivise new mines. An analysis by The Silver Institute suggests that the average All-In Sustaining Cost (AISC) for primary silver producers was US$26.86/oz in 2024, and with global silver prices only moving above US$30/oz sustainably this year, it’s really only been in the past six months that many development projects could realistically approve a FID.

And with silver a hard rock mineral, one has to think that it will take at least two to three years to build new capacity, which means that we won’t see substantial new primary supply coming into the market until 2028 at least.

Above-ground inventories are declining

The lack of new supply is going to be an issue because of the fact that silver inventories have been in decline in recent years.

Now, unfortunately, the inventory picture is much more complex in silver than in many industrial metals because of investment demand for silver. Investors in silver can buy any one of a number of products of which the two most important in my view are:

- Direct investment through purchasing of silver bars

- Purchasing of exchange-traded products which hold physical silver

We can track silver inventories like we can track inventories for most industrial metals. So there is a COMEX series, and a SHFE series. But there are also other sources of inventories.

In China, there’s also the Shanghai Gold Exchange (SGE). Up until recently this has just been for investment in silver, but recently it has started to make material available to physical users of silver as well.

And then there’s the London Bullion Market Association (LBMA) which tracks silver inventories in the London markets. Historically the LBMA has been the largest source of global silver inventories. But with LBMA we have to be careful about overstating inventories.

And that’s because of the second class of investments I highlighted above, exchange-traded commodities or ETCs. Now ETCs can take two forms; those that are settled on paper markets and those that are settled on physical ones. And it just so happens that in silver there are a growing number of ETCs which invest in physical metal. And at least four of the largest ETCs store their metal in London.

In basic terms, metal that’s tied up in an ETC is not available to be supplied to end use markets because the owner of the ETC wants to own that physical metal.

Global ETCs currently represent over 800Moz of silver and ETCs that warehouse their material in London represent c.570Moz of material. So that material needs to be backed out of LBMA inventories. The chart above understates ETC inventories but we use the iShares Physical Silver ETC (SILV) as a proxy because of its easily-available history. I also note that monitoring silver inventories is made more difficult by the fact that the LBMA only releases monthly updates while all other major exchanges release weekly and even daily numbers. Given quite a lot of destocking this month, it’s likely that the chart above overstates available inventories quite considerably.

The last 7-8 years have seen a substantial drop in the amount of silver inventories available in the market and, even though inventories built somewhat over the course of 2025, in days of consumption terms they are still low compared to recent history.

The difference between paper and physical markets

The most followed silver price in the world is the COMEX silver future. But that doesn’t tell you the whole story. In fact, many silver market specialists suggest that it tells a totally different story to the actual state of the physical silver markets!

Over the past few weeks, the COMEX silver futures price rose above US$50/oz and then crashed down. But physical silver prices in China and India stayed elevated, suggesting that there are different drivers at play in physical markets as compared to paper markets.

And I would suggest that there are. Because I believe paper silver traders are still looking at things like the Gold/Silver ratio and macro indicators for the silver price, whereas silver is becoming an increasingly-important material for industrial uses. And industrial inventories are heading south at a rapid rate.

And that results in situations like we’ve seen over the past few weeks where industrial and investment demand for physical silver remains very strong even as paper traders push the silver price lower. Everything I know as an industrial materials analyst for the past 20 years says to me that silver is heading for the mother and father of all structural shortages, but paper traders just don’t see it. Or perhaps, as many suggest, they are simply manipulating the price lower?

Paper traders have been happy to take profits after silver has risen 50% for the year. My experience as an industrial metals analyst suggests that silver prices could be multiples of their current level within a few years.

I’m sure I’ll be writing more about silver going forward. But if you’d like to find out more about my thoughts on solar installations and silver demand, have a look at my recent Blog article. Until then, do yourself a favour and start looking at the silver market in more detail, because I think it has the potential to be the next big thing in critical materials.