It’s been an exciting two weeks in the lithium market, with the second price spike this year and a number of brokers seeming to start to catch up with the huge growth in ESS installations and to adjust their demand forecasts upwards.

Some brokers have moved from bearish to bullish, while some have doubled down and remain bearish on lithium.

I’ve watched most of the reports break across social media and seen the shocked, surprised and sometimes disparaging opinions on the analysis (or sometimes lack of it!) contained in the reports. By the nature of my role I’ve had the opportunity to read many of the reports as well.

Supply tracking a real bugbear

One of the things that’s been a real issue for me in recent years as I’ve looked at the lithium market has been the extent to which many brokers have visibility on Chinese supply. I’ve seen a lot of reports coming across my desk that I don’t believe are realistic in terms of how much Chinese supply growth is being forecast. And, again, that’s been an issue in the current publishing cycle as well.

In line with this I decided to go in and do some work on which brokers were forecasting what supply and from where.

Which is when I discovered what is perhaps the biggest problem in lithium analysis at the current time.

What is the right number?

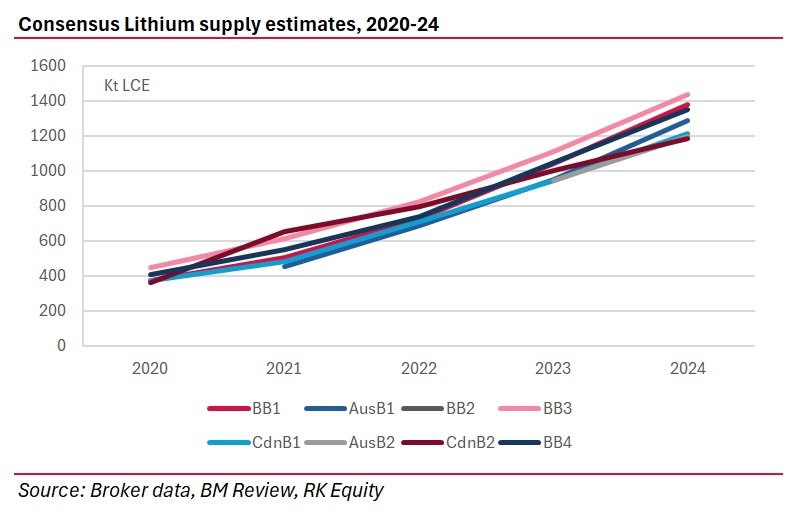

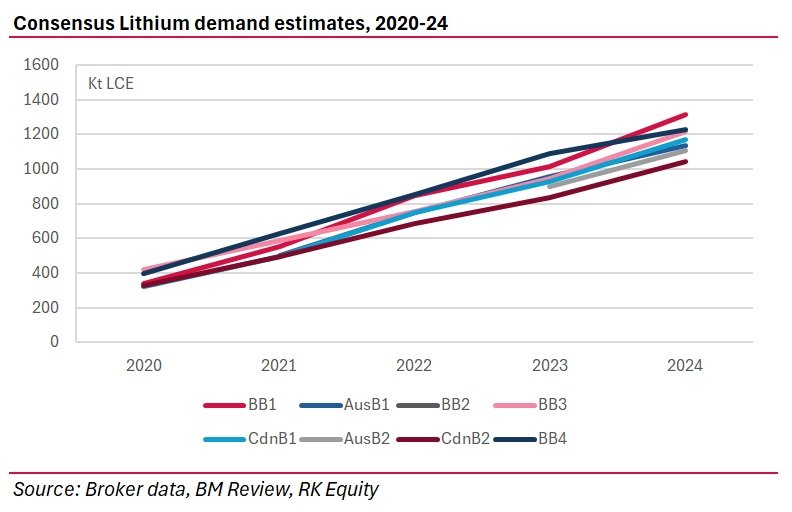

I’ve been through reports from ten different brokers published over the past six months. These vary from global bulge bracket banks (BB), to regional Australian brokers (AusB) and Canadian brokers (CdnB).

It’s probably not a surprise to anyone that there’s a substantial difference in the forecasts for each of these ten brokers on both supply and demand.

But what probably will be a surprise to everybody is that there is also a huge range in the historical data being published by each broker. In fact in the years 2020-24 there is on average a 25% deviation between the high and low numbers for supply, and a 28% deviation between the high and low numbers for demand.

That simply should not happen and doesn’t happen in any other material that I’ve worked in over the past 25 years of my career – be it chemical, metal or paper. You might see a 2-5% range in historic numbers, but not +20%!

What does that mean in actual terms? For instance, if we look at supply, in 2024 one bulge bracket broker said that supply was 1439Lt LCE, whereas one Canadian broker had it at 1184Kt LCE. Who is right?

And this is the problem with the lithium market. We don’t know. But a difference of 22% can have a substantial impact on how we forecast the supply/demand balance, going forward.

The difference is just as substantial in terms of demand. In 2024 the demand range is 1045Kt LCE to 1312Kt LCE. Again, we don’t know who is correct because there’s very little transparency in the market. If I take a c.20% demand growth forecast for 2026E and whack that on those two numbers, it’s translating into an even greater deviation.

We need some central body (like the International Lithium Association) to come in and vet these supply and demand numbers and tell us what the historic data should be. Because without knowing what the actual historic data is, it’s practically impossible to understand what impact forecasts will have on the market and pricing.

Think about it; if broker A comes out and says I forecast demand in 2026E at 1.8Mt LCE, one might get really excited and say – ‘well that’s up 80% from the 2024 level!’ but actually it might only be up 38% from the 2024 level that they’re using…

Similarly, it’s difficult to get an idea for what the actual market balance is if one broker’s supply forecast is 25% different from another’s and you’re using a third broker’s demand forecast which is also based on different levels…

How can anyone take a view on what absolute lithium demand (or supply) will be in 2030 if no one can agree on what it is now?

As it stands at the moment, all broker Supply/Demand analyses have to be taken separately and individually because they’re not fungible across the industry. And that’s a bad situation to be in. It makes it very difficult for generalist investors to get their heads around the industry and, as I’ve said before, I firmly believe that this sector will succeed or fail according to the amount of generalist capital it manages to attract.

The industry needs to get its act together. And fast.