You can’t get around the fact that the main driver of growth in the battery market over the past 12 months has switched away from EVs and to ESS. And ESS demand is starting to go mainstream, with a number of brokers upgrading their lithium demand forecasts over the past six months, based on their increasing understanding of the potential for ESS demand. Better late than never, I guess!

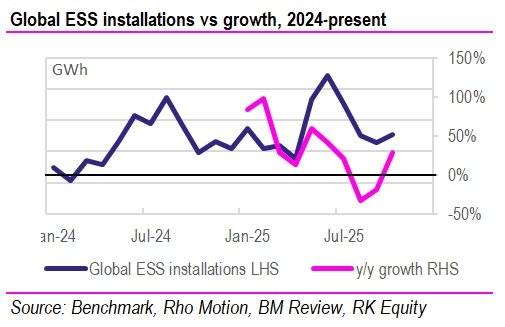

But there is something of a bifurcation in the ESS market at the moment, and it’s a very important one. If one looks at ESS cell production or shipments (ie supply) it’s growing very rapidly; perhaps not quite at the rate that it was growing towards the end of last year and the beginning of this one, but still very fast.

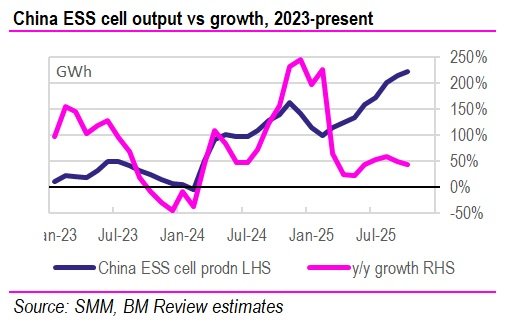

The adjacent chart shows that Chinese ESS cell output has risen from 38GWh per month in October 2024 to 54GWh per month in October 2025 and just keeps on growing! And we’re seeing cell production lines in the US, Europe and Japan being converted to produce ESS cells as well.

And analysts that track ESS shipments are, understandably, very bullish indeed on ESS demand.

But there is a bit of a problem with basing demand forecasts solely on ESS shipments. The problem is that ESS installations are not growing nearly as fast as shipments are. Now, one caveat with this; it’s pretty difficult to get reliable data on ESS installations on a global basis. The only freely available data is Benchmark/Rho Motion’s global installation database which, I understand, only covers utility-scale ESS installations.

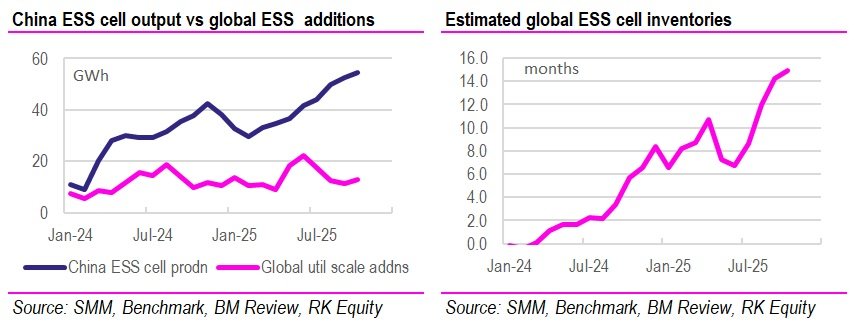

Now obviously, if we’re comparing ESS output with only utility-scale installations, we’re understating demand but, if I plot the two lines on the same axis (as below), I think you can understand the issue that I’m highlighting. For my inventory calculation I apply a monthly adjustment to add approximate Residential, as well as Commercial & Industrial (C&I) demand for ESS batteries. And because, in rapidly-growing markets, I’m not a fan of looking at inventories in absolute terms, I divide by current demand, to show global BESS inventories in days of installation terms.

And you can see pretty clearly that there’s been a big build in ESS cell inventories in the second half of this year.

Where are these inventories sitting? you may ask. Because anecdotal reports suggest that it’s still very difficult to buy ESS batteries in China currently. I would suggest that the inventory is sitting mainly with the consumer. We already know that US utilities and integrators built up significant inventories of Chinese LFP cells at the end of 2024 because they were worried about President Trump’s stated aim of tariffing Chinese shipments (which has, in fact come to pass). I would suggest that there is some concern in the industry also about the potential for lithium-ion cell prices to increase, given the recent move in lithium chemicals prices as well. There may never be a better time to build up inventories of Chinese LFP ESS batteries than the second half of this year, and it definitely seems that many consumers have made hay while the sun shines!

Now, the big question is – how high is too high? And I’m not sure I have an answer to that. Is it 12 months, is it 18 months, 24 months, or is it longer, given the potential for project delays in some regions? I don’t know, but I’m pretty sure that the industry will tell us when the right time is – it’ll be when users stop buying ESS batteries! But it’ll come on very suddenly with not much notice. Just as we experienced in 2022-23 when cell, cathode and chemicals inventories reached the industry’s choke point.

Just to be clear, I’m not saying that ESS inventories are at scary high levels and the market is going to correct. I’m saying that ESS inventories are building and, if they continue to build at this rate, we’ll see a correction somewhere down the line. And investors need to keep an eye on ESS demand because it won’t go up in a straight line. As with all cycles, there will be occasional corrections.

So this is just an advisory to keep an eye on this very important data point.

For now, ESS continues to go gangbusters, and that’s positive for lithium demand in the context of slowing growth rates in EV sales. Hopefully it continues for some time yet.