On 9-10 October 2025, in response to what it saw as trade provocation from the US, China broadened its rare-earth export controls, expanding restrictions on a number of materials and technologies. The US response was immediate and, by mid-October, the Western press was reporting that a trade deal between the US and China on critical materials was imminent. Said deal eventually emerged on 30 October 2025.

Many stocks of critical minerals developers saw widespread sell-offs as the market seemed to interpret the deal as a final one that de-risked critical materials supplies globally. But, as I observed in the November edition of Battery Materials Review, in my view this couldn’t be further from the truth.

Let’s be very clear about the deal. It delays the worst of the Chinese measures for maybe 12 months. It’s not a final deal; it just kicks the can down the road. And does it remove the risk of China throwing its collective toys out of the pram in the critical minerals supply chain at a later date? Absolutely not.

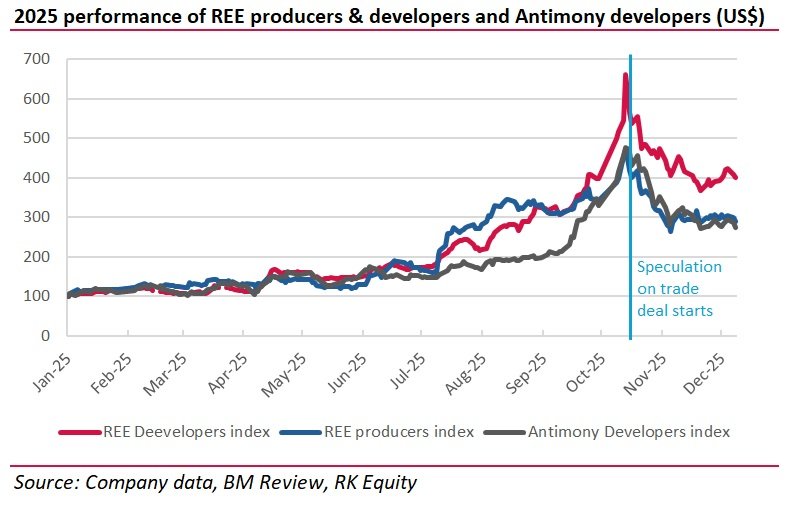

But prices of critical materials stocks have reacted like it does. And in two segments in particular there has been a huge equity sell-off, which is not justified, in my view. I’m talking about antimony and rare earths. In these segments, stocks with development projects, and some producers, are down 30-40% since mid-October. This seems completely unjustified to me.

REE: China still controls value chain

According to the US wording of the deal between the US and China, “China will suspend the implementation of the new export controls on rare earths and related measures”. According to the Chinese wording, this is only for 12 months.

So, does that means that the trade tension between the US and China over Rare Earths is over? No it most certainly does not, in my view.

There’s been a lot of fanfare about a succession of deals that the US has done in the permanent magnet supply chain but, so far, the bulk of those deals (with the exception of MP Materials and Cerro Verde) seem to be in the Downstream part of the segment and not in the upstream.

I’ve seen a lot of “experts” opining that that’s because Rare Earths are not, in fact, rare. And that’s true. They’re not particularly. But economically extractable reserves of rare earths are pretty rare. And economically extractable reserves of heavy rare earths are extremely rare. And that’s a problem, because there’s been by no means enough investment in upstream projects in heavy rare earths to wrest control of the value chain away from China.

And the other issue is that, apart from Lynas and MP Materials, the rest of the next tier of developers are mostly small-cap (ie less than US$1bn market value). And small caps are generally extremely reliant on the equity market for capital to fund project evaluation and development.

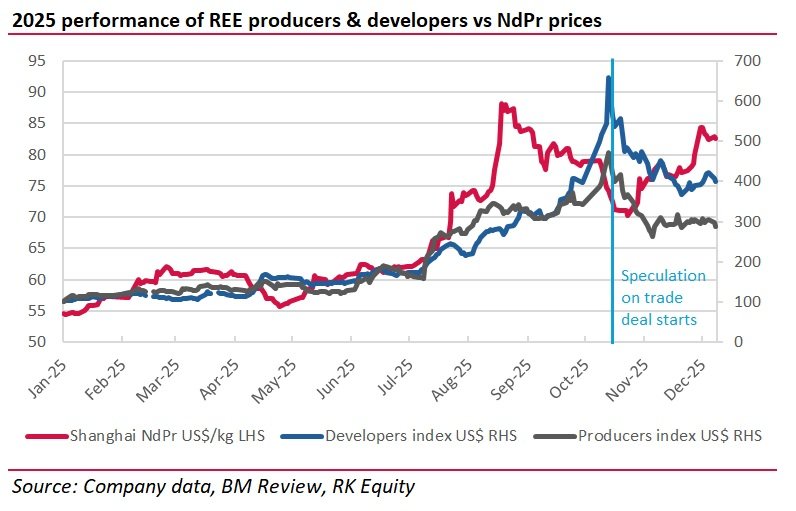

So the magnitude of the collapse in share prices could have substantial implications in terms of the sector’s ability to fund the next stage of projects. Which puts us kind of back where we were before the trade deal. And, as the chart below shows, Rare Earth prices haven’t fallen since October. In fact they’ve increased. So why have stocks corrected to such an extent? It’s not justified and it likely presents a very strong buying opportunity, in my view.

Stocks in our REE developers index: Viridis Mining & Minerals, Brazilian Rare Earths, Lindian Resources, Arafura Rare Earths, Meteoric Resources, Aclara Resources, Rare Element Resources, Ucore Rare Metals, Pensana.

Stocks in our REE producers index: MP Materials, Lynas Rare Earths.

Antimony: Market running scared of Chinese exports

In the announced trade deal one phrase seems to have the market running scared of antimony stocks, and that’s “China will issue general licenses valid for exports of rare earths, gallium, germanium, antimony, and graphite for the benefit of US end users and their suppliers around the world including the de facto removal of controls China imposed since 2023”.

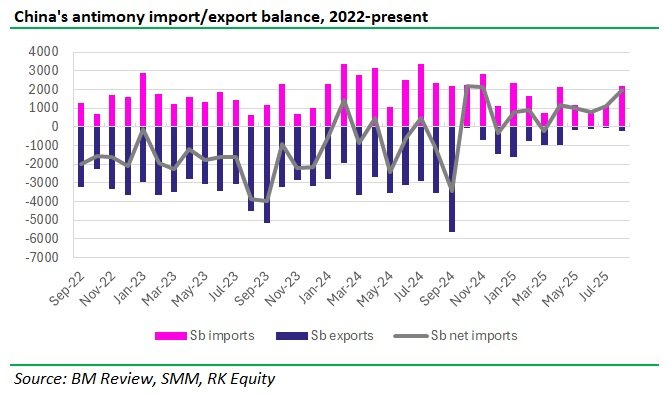

Of course, that just means that China agreed to issue export licences; it doesn’t mean that it necessarily will export material. I’m not actually convinced that China has the ability to export large amounts of antimony. As I noted in a previous blog article, Chinese domestic demand for antimony has gone through the roof in recent years thanks to demand from the solar industry. Chinese exports had already tailed off some time before the export ban and I’m not really convinced that China will be able to export large amounts of antimony, even if it nominally could do so.

The chart above shows that exports collapsed in August/September 2024, even before China announced that it was halting exports. I suggest that China halted exports as much because it didn’t have excess material to export as anything else. Given the growth in solar panel output in China in the intervening years, it seems highly-unlikely that more material will be available.

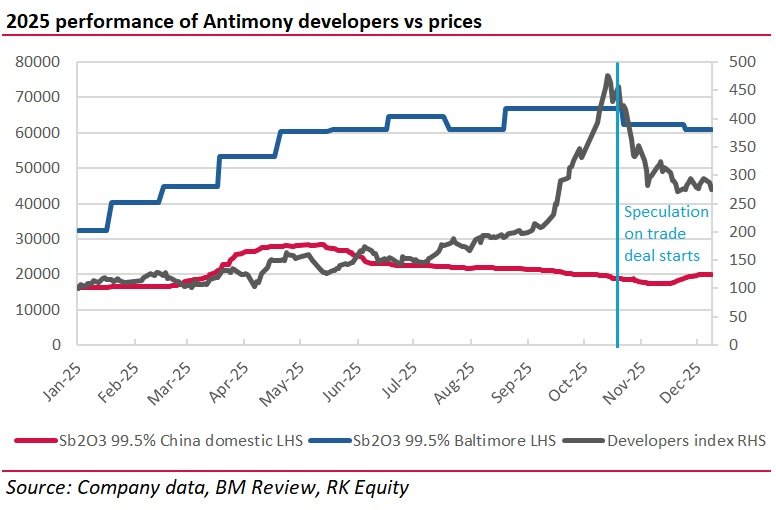

This means that again the stock market has over-reacted, in my view. The chart below shows that our index of antimony developer stocks has sold off by 41%, with some stocks selling off by up to 55%, while the Chinese domestic antimony price rose by 4% (after initially falling slightly) and the Baltimore warehouse price fell by 9%.

Obviously time will tell if China does resume exports but it already stated that it won’t export material for military applications and that is a key segment where the US needs material. Absent Chinese exports, some of these US development projects will therefore need to get developed.

This also looks like a segment where the sell off is overdone, in my view.

Stocks in our antimony developers index: Canagold Resources, Felix Gold, Larvotto Resources, Perpetua Resources, Trigg Minerals, United States Antimony.