Rare earth magnets sit at the heart of electrification. They are used in EV traction motors, wind turbines, robotics, drones, industrial motors and many other high-performance applications. The key magnet type is NdFeB — neodymium-iron-boron — which is powerful, compact and efficient.

After the industry has been flagging China’s dominance in Rare Earth minerals for over ten years, politicians have finally started to take notice in recent years and, over the past 12 months, we have seen both the US and Japan look to try to lock in supply of key rare earth magnet materials.

When we talk about magnet materials, we’re normally talking about four key elements: neodymium, praseodymium, dysprosium and terbium. These are often known as the magnet rare earths.

Neodymium (Nd) and Praseodymium (Pr) generally make up c.80% of the economics of a rare earth project. They are actually what is known as light rare earths or LREE, while the other two elements, dysprosium (Dy) and Terbium (Tb) are part of the heavy rare earths (HREE) chain.

While there is quite a lot of NdPr in most rare earth deposits, Dy and Tb are an order of magnitude more rare. That has resulted in huge investments in exploration for Dy, Tb and other HREEs (many of which are vital in defence applications) in recent years.

Therefore it was quite a surprise for many to hear on MP Materials’ Q1/26 earnings call, its CEO James Litinsky being quite down on DyTb. He said he “wouldn’t be surprised” to see prices for magnetic HREEs (DyTb) “decline materially”.

Why would MP Materials’ CEO say this and what caused him to make these comments? After all, Nd, Pr, Dy and Tb are all needed for rare earth magnets aren’t they? If we’re positive on rising demand for rare earth magnets, why wouldn’t demand for DyTb be huge?

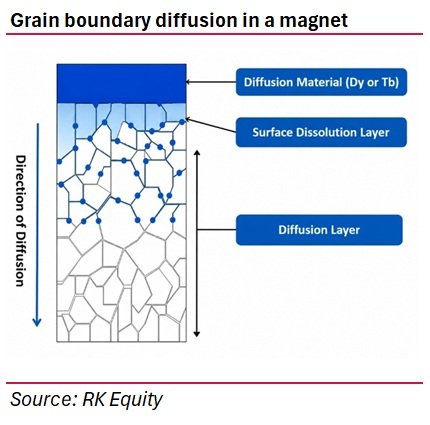

Well, I haven’t had a chance to speak to Litinsky, but I would say that the basis for his comments comes down to something called Grain Boundary Diffusion (GBD).

What is GBD?

In traditional high-performance NdFeB magnets, Dy and Tb are mixed into the magnet material itself. Think of it like putting an expensive ingredient through the entire cake mix.

GBD changes that recipe. Materially.

Instead of mixing Dy and Tb throughout the whole magnet, producers apply smaller amounts of DyTb-rich material to the surface of a finished magnet and heat it. The Dy and Tb then move along the tiny boundaries between the magnet grains. In simple terms, the expensive material is put mainly where it does the most useful work: around the edges of the magnetic grains, where it helps the magnet resist demagnetisation at high temperature.

GBD therefore raises coercivity – the magnet’s ability to resist losing magnetism, without sacrificing as much magnetic strength as traditional bulk DyTb addition. Magnet specialist SM Magnetics has stated that GBD distributes heavy rare earths into the intergranular material around the grains, while the traditional method mixes Dy and Tb into the initial grain structure, which can improve coercivity but reduce induction, or magnetic strength.

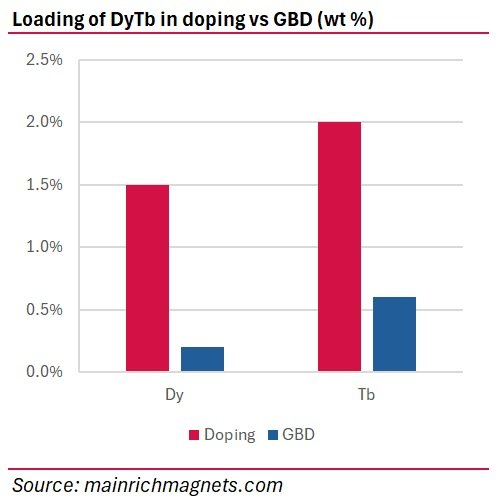

GBD reduces DyTb usage per magnet

The old approach is effective but wasteful. Much of the DyTb ends up inside the grains, where it is less useful. GBD targets the grain boundaries instead creating thin DyTb-rich shells around Nd₂Fe₁₄B grains rather than loading the entire bulk alloy.

Industry commentary points to a broad reduction of around 50–70% in DyTb usage on each magnet for equivalent high-temperature performance vs traditional doping, while maintaining similar performance.

That is a big deal. For example, if an older high-temperature magnet used 5% DyTb by weight, a GBD version might use closer to 2%. The magnet still gets the heat resistance it needs, but with much less HREE material.

But GBD does NOT eliminate DyTb demand

And this is the core point for investors.

GBD reduces intensity – the amount of DyTb per tonne of magnet. It does not remove the need for DyTb altogether. In the highest-temperature applications, particularly more-demanding EV motors, aerospace, industrial motors and some wind applications, Dy – and especially Tb – still matter.

There is also a geometry issue. GBD works from the surface inward. That means it is best suited to thinner magnets or segmented magnet designs. SM Magnetics notes that diffusion does not penetrate throughout the entire magnet volume and that this can create uneven coercivity through the magnet, especially if the process is applied to a sintered block.

So GBD is not a magic wand. It is a powerful thrift technology. It makes what is currently a very limited supply of DyTb go further.

The demand paradox: less per magnet, more magnets

So it’s true. GBD does lower the amount of DyTb needed for each magnet. And, if magnet demand were flat, GBD would be bad news for DyTb demand.

But magnet demand is not flat. Not by a long way.

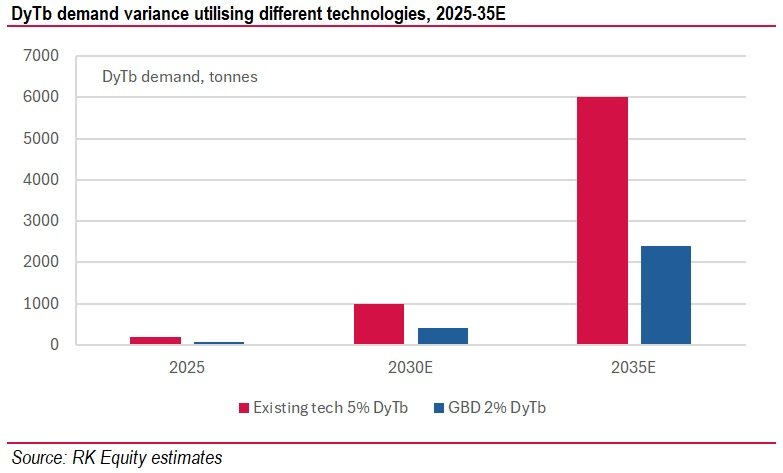

Between autonomous vehicles, humanoid robots and VTOLs, most analysts suggest that demand for rare earth magnets could grow 5x between 2025 and 2030E and over 30x between 2025 and 2035E.

The chart below illustrates what that could do to DyTb demand using the current technology and using GBD.

GBD dramatically lowers DyTb use per tonne of magnet. In the 2035 example, it cuts potential DyTb demand from 6,000 tonnes to 2,400 tonnes per year. That is a huge saving.

But 2,400 tonnes is still 12x the 2025 old-technology requirement of 200 tonnes and 30x what DyTb demand is estimated to have been in 2024. In other words, GBD slows the growth in DyTb demand, but it does not remove the structural supply challenge if magnet volumes rise as expected.

And, by the way, you’ll probably have noted that DyTb demand in 2024 is closer to the assumed demand level for GBD in 2025 than to demand using the old technology. That’s because most Chinese magnet manufacturers have already switched to GBD. And, since China dominates magnet manufacturing, that means that most magnet manufacturers have already switched to GBD.

Investment takeaway

In my view, GBD is a great thing for the industry. The Rare Earth industry is already struggling to be able to add enough capacity to even cope with near-term magnet demand. It will be a struggle for the mining industry to even hit 2030 HREE demand targets incorporating GBD, in my view. It would have no chance of hitting the old tech demand targets.

And, unfortunately, I’ve seen industries where demand substantially exceeds supply and prices spike as a result. They tend to experience technology change and demand destruction. So the fact that demand targets are lower – at a level that the industry might actually be able to attain – is a great development in my view.

But the point is that the industry could still see a 30x increase in DyTb demand between 2025 and 2035. That’s going to be difficult to supply.

So we still need prices to rise, governments to continue to invest in rare earth supply and investors to invest in the Rare Earth industry. And, with a 30x increase in demand for DyTb on the boards, I can’t see a situation where prices will fall in the medium-term, despite what MP Materials’ CEO suggests.